Learning Market N° 3: Chainalysis State of Web3 Report

Learning Market N° 3: Chainalysis State of Web3 Report

Summary of the Chainalysis 109-page State of Web3 Report.

This is the 3rd edition of the “Learning Market”, a series that I launched to share some of the content I read and listen to.

Instead of focusing on crypto prices, this is the perfect time to study, learn, and be one step ahead of everybody else when the next bull run hits.

I read the Chainalysis 109-page State of Web3 report. Here’s the summary.

1. INFRASTRUCTURE

One day in the near future, all companies will become crypto companies,

complete with a “Connect wallet” button on their homepages. And web3 is

how they’ll get there.

Web3 cases:

Finance

Fractional ownership of physical assets

Eliminate Middlemen (web2 platforms for example)

Enables community ownership of companies (DAOs)

Where we are now and what happens next

Bitcoin accounted for the majority of crypto transaction volume as recently

as 2016, but so far in 2022, represents just over 10%. Stablecoins account for much of that, but cryptocurrencies with the smart contract functionality that powers DeFi and web3 now account for 45%.

Problem: DeFi adopters tend to be already established cryptocurrency users - with the expectation of NFTs, which attracted many users.

How can our industry capitalize on this momentum and build toward

the ultimate vision of web3?

Onboard more new users into cryptocurrency generally

Better user experience for cryptocurrency and web3 tools.

Address use cases non-crypto natives care about.

Layer 1 Blockchains

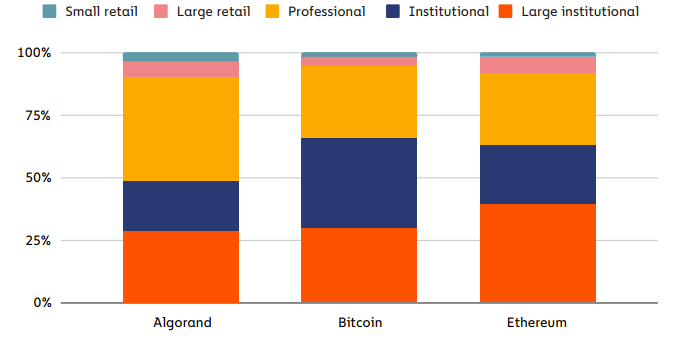

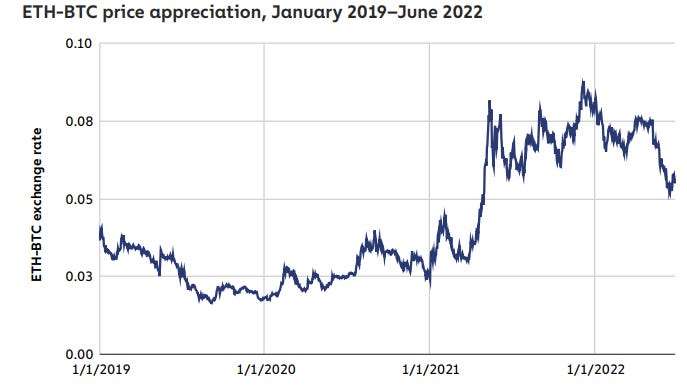

Ethereum stands out as the cryptocurrency with the most institutional dominance.

The rise of DeFi 2021 appears to have sparked a huge increase in investor sentiment for Ethereum relative to Bitcoin.

Other L1s

Solana

Uses a unique consensus mechanism that combines PoS with Proof of History (PoH). PoH seeks to solve the issue of timestamping transactions that occur on a blockchain, which determines the order in which validators confirm those transactions.

Algorand

It has a two-tiered blockchain structure. The base layer supports basic

transactions, as well as smart contracts for new tokens and atomic swaps.

The second layer, on the other hand, is reserved for more complex smart

contracts, such as those powering dApps. This bifurcation of the Algorand

blockchain enables Algorand to process transactions efficiently.

Algorand uses a variant of PoS called Pure Proof of Stake (PPoS), with much lower staking requirements than other PoS blockchains.

BNB Chain

BNB Chain is a blockchain launched by cryptocurrency exchange Binance, with BNB being its native token. BNB Chain can’t be said to be fully trustless – in the technical sense — as it’s maintained by a centralized, legally incorporated business entity.

Avalanche

Avalanche touts itself on three key attributes:

• Customizability to build a variety of dApps and tokens.

• Scalability thanks to low fees.

• Interoperability to interact with other blockchains.

Avalanche says it can be a “platform of platforms” and support significant Layer 2 development.

Avalanche accomplishes this with a set of three blockchains, each serving different use cases:

• C-Chain executes transactions related to Ethereum-native dApps, and

is currently the most-used of the three blockchains.

• X-Chain allows for the creation and exchange of new assets built on

top of the Avalanche blockchain

• P-Chain coordinates the Avalanche blockchain’s validators and the

creation of subnets.

The future of Layer 1s

Ethereum is still far ahead in transaction volume, especially in popular areas of web3

like NFTs, and the Ethereum Foundation is working with miners to implement

changes to address its issues. The upcoming Ethereum 2.0 upgrade, which will

see Ethereum switch to a PoS consensus mechanism and implement sharding

to process a higher number of transactions in parallel, is expected to increase

Ethereum’s scalability and lower gas fees. If Ethereum’s entrenched status

as the number two blockchain behind Bitcoin is already allowing Ethereum

to fend off competitors, it seems especially unlikely that another smart

contract-enabled blockchain will challenge it should these changes prove

successful.

It’s possible that investment in alternative Layer 1s slows down, and that web3

becomes a winner-takes-all market, with Ethereum as the dominant player.

Digital Identity

One of the biggest shortcomings of web2 is the precarity of consumers’ data

security and privacy. Web3 can help solve this problem by disentangling payments and customer-business relationships from real world identity except where absolutely

necessary.

Ethereum Naming Service (ENS)

By integrating with IPFS, ENS domains can represent these decentralized

websites as well as Ethereum addresses. The combination of ENS and IPFS can go beyond addressing privacy and security concerns, and may represent the beginning of a more democratized, bottom-up internet, in which users and creators can interact free of middlemen, censors, and other third parties.

The ENS-ICANN integration could prove to be a crucial bridge from web2 to

web3, and at the very least makes it easier for web2 businesses to accept

cryptocurrency payments and expand their customer targeting to crypto

natives

2. DeFi

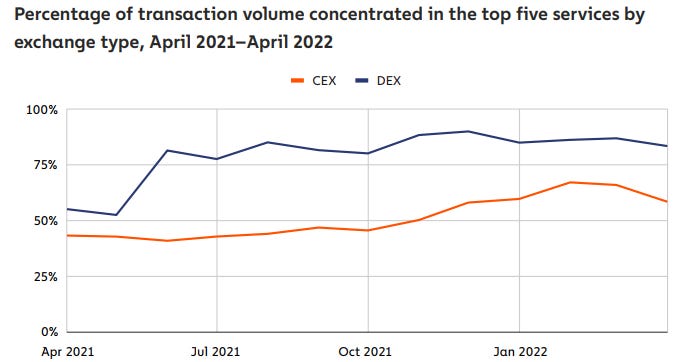

While most CEX transactions happen off-chain on centralized databases and

captured on their order books to save on transaction fees, every DEX transaction occurs via smart contracts on-chain. For this reason, as well as the

rapid growth of DeFi generally, DEXs now have a confident lead in on-chain

transaction volume: from April 2021 to April 2022, $175 billion was sent

on-chain to CEXs, well below the $224 billion sent to DEXs.

The top five DEXs concentrate more volume than the top five CEXs. There are three reasons for this:

DEXs’ recent emergence. Without as much time on the market, fewer DEXs have been able to establish themselves and sustain an active user base.

economies of scale: DEXs with higher liquidity may be able to provide more stabilized pricing for even the biggest market participants, but smaller pools may struggle to do the same without causing considerable price slippage — an

unappealing proposition for both consumers and liquidity providers.competition is intense

Centralized exchanges’ lower concentration may be due to greater competition among CEXs, greater focus on regulatory hurdles within and across jurisdictions, and/or greater variability in how much these services’ users also use personal wallets.

How much do DEX users earn for providing liquidity?

Users who fund these AMM-style DEX pools are known as liquidity providers

or LPs. In exchange for filling these pools with cryptocurrencies, LPs collect

transaction fees on any trades that use their liquidity.

How much do LPs earn?

The fees earned by LPs are closely tied to DEX transaction volumes. On a

monthly basis, fee earnings have fluctuated between $50 and $150 million,

a small fraction (0.05% to 0.3%) of the $50 to $300 billion that has flowed

through these exchanges during the same period.

Generate Yield: Lending and Staking

Staking provides rewards and powers proof of stake consensus mechanisms

Just as miners create mining pools to combine their computing power and

maximize their chances of mining new blocks, stakers can also gather into

staking pools to do the same thing. Staking pools make it easy for any holder

of the relevant blockchain’s assets to participate in validation and earn

rewards — all they need to do is send their tokens to the pool’s address, and

the pool operator does the rest.

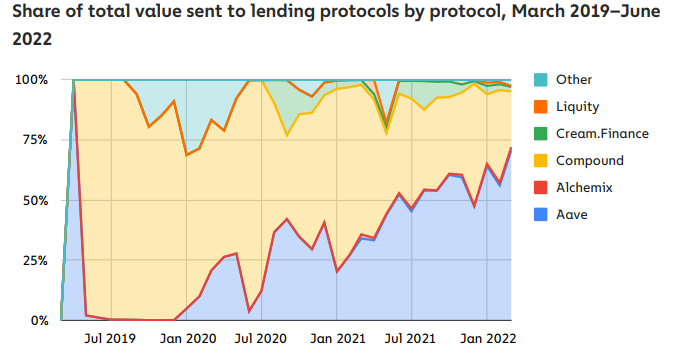

Lending: Users send cryptocurrency to the protocol’s pool, and similar to staking, receive tokens minted by the pool of equivalent value to what they put in, as well as rewards generated by their deposit.

AAVE is the leading lending protocol:

84% of funds borrowed from lending protocols go to other DeFi

protocols. Problem: Leverage —>If users invest borrowed funds

in another risky, high-yield DeFi protocol, and that protocol fails, those users

may be unable to pay back their loans — if that happens to too many users

at once, the original lending protocol can become insolvent

Enjoying the summary so far? Please consider subscribing, it’s free!

3. DAOs

Problem: governance token data suggests that DAO ownership is highly concentrated. across several major DAOs, less than 1% of all holders have 90% of voting power.

For a governance token holder, there are three key governance actions. Voting

is simple — any holder can do it. But what about creating a proposal? And

what about passing it?

Per these ten DAOs proposal requirements, we find that:

1. A user must hold between 0.1% and 1% of the outstanding token supply to

create a proposal.

2. A user must hold between 1% and 4% to pass it.

Using these ranges as lower and upper bounds, we find that between 1 in

1,000 and 1 in 10,000 of these ten DAOs’ holders have enough tokens to

create a proposal.

Overly concentrated voting power in DAOs can result in decision-making that

seemingly contradicts the tenets of decentralization on which web3 is built.

In terms of the number of DAOs and their treasury sizes, however, DeFi-related DAOs have a giant lead. The DeFi category accounts for 83% of all DAO

treasury value held and 33% of all of the DAOs by count.

38% of on-chain DAO treasuries have correlations with Bitcoin that are

between 0.5 and 1.00.

Who contributes to DAOs?

DAO participants are advanced users of cryptocurrency services.

4. NFTs

Since the beginning of 2021, NFT transaction volume has grown significantly,

but this growth fluctuates.

if we think in terms of transaction value rather than number of

transfers, we see that NFT collectors make up a majority of activity. Institutional investors are nipping at their heels, and even make up the majority of

activity in certain weeks when extremely large purchases have been made.

The growth of institutional-sized NFT transactions hasn’t been consistently sustained.

5. Metaverse and Gaming

For artists, brands, and gamers, the metaverse is a living reality.

Blockchain-based virtual real estate (VRE) offers both present-day and

prospective benefits to the people who own it:

Present-day utilities

• Embedded videos, images, NFTs, and interactive objects

• In-game single-player and multiplayer activities

• Play-and-earn integrations

• Screen-sharing and town hall functionalities

• Access to private events and NFT-gated communities

Prospective utilities

• Renting and leasing

• Free airdrops of future VRE NFTs

• Future AR/VR integrations and functionalities

The long-term value of blockchain-based VRE depends on a number of external factors:

Whether AR/VR systems are more interoperable or proprietary

To what extent will the big companies’ technologies be open-sourced and accessible to build upon? And will they allow other metaverse

companies to connect their projects, or will they create a walled garden

within which only they can develop?

In June, big-name tech companies like Meta, Microsoft, and Epic Games

formed the Metaverse Standards Forum (MSF). This group is meant to create

open standards for all things metaverse, including AR, VR, and 3D technology.

2. The pace of adoption of new computing technology

The more immersive and life-like the virtual experience, the more likely it is for

NFT-based ownership to feel tangible to users. So the faster VR technology

grows, the better it is likely to be for metaverse land offerings.

VR and blockchain technology as two of the five key metaverse building blocks:

1. Operating systems connecting people and content

2. Blockchains that decentralize economic systems and digital asset

ownership

3. Natural user interfaces e.g., voice control and gestures for greater

user immersion

4. Extended reality (XR) headsets

5. Cloud networking infrastructure.

Blockchains and gaming

Blockchain-based gaming activity has increased 2,000% over the last year .

What would happen if EA Sports became a web3 gaming company?

Financial model for both EA’s revenue and Ultimate Team players’ earnings in a game mode reimagined with NFTs:

Introducing NFT player cards could generate significant additional revenue for EA Sports and could create a first-of-its-kind market for players to profit.

Primary sales would still be EA’s main revenue driver. But the secondary sales, while accounting for only a fraction of EA’s $1.87 billion in revenue, would benefit players immensely.

6. Safety and Compliance

Illicit DeFi transactions have risen steadily over the last three years, in terms

of both raw value and also as a share of all transaction value. We see this

primarily in two areas: Theft of funds through hacking, and abuse of DeFi

protocols for money laundering.

Over the course of 2021, DeFi protocols became the go-to target for hackers looking to steal cryptocurrency. DeFi protocols account for 97% of the $1.68 billion worth of cryptocurrency stolen in 2022.

DeFi protocols have become the biggest recipient of illicit funds, taking in 69% of all funds sent from addresses associated with criminal activity, compared to 19% in 2021.

Wash trading is a form of market manipulation in which a seller is on both sides of

a trade — in other words, selling an asset to themselves — in order to create

a misleading perception of that asset’s value or liquidity. Wash trading is

relatively easy to do with NFTs, as some NFT trading platforms allow users

to trade by simply connecting their wallet to the platform, with no need to

identify themselves. One user could easily control multiple wallets and trade

NFTs between them, and no one could know unless they took the time to

analyze the wallets’ transaction histories.

Mitigating Financial Risk

Cryptocurrencies — especially Bitcoin, the most established cryptocurrency — are now more correlated to tech stocks than they were in the past.

This correlation reflects crypto’s maturity as an asset class: there are a

growing number of institutional players involved, new types of financial

products are being offered, regulatory oversight is developing, and the

market is more efficiently pricing in new information.

Due to the open nature of DeFi protocols, the market can often see where large, well-known players placed their bets and if those positions are facing liquidation. Furthermore, market participants can use this transparency to assess the stability of the core protocols that power the DeFi ecosystem.

However, this transparency has not stopped large, centralized companies

from making bets on the price of various cryptocurrencies, both using open

DeFi protocols and by lending funds to one another. This creates potential

contagion risk, as various centralized market participants are financially

exposed to one another.

Previous Editions of The Learning Market:

Learning Market N°2: Fantastic Macro Article by Lyn Alden

If you enjoyed this ad-free and zero-cost content, please follow me on Twitter @JuampiAranovich and Subscribe to the Newsletter