Fidelity's Take on ETH Left Me Pondering

Fidelity's Take on ETH Left Me Pondering

...but not for the reasons you might assume.

Fidelity recently unveiled their investment thesis on Ethereum, and I must say, it left me with a raised eyebrow. But before we dive into my reflections, let's break down the essence of their argument. They dive into:

Ethereum's dual role as a technology platform and a payment system, with evolving value dynamics post The Merge.

The distinction between the Ethereum network and its native token, ether, with recent alterations reshaping its economic model.

Ether's value generation through mechanisms like base fee, priority fee, and maximum extractable value (MEV).

Ether's position in the space, sharing certain properties with bitcoin but differing in scarcity and historical trajectory.

The potential regulatory challenges Ethereum faces, especially in the U.S., and its stock-to-flow ratio.

The anticipation of future supply influences and the emergence of a multi-chain economy with different blockchains serving various use cases.

Ether's role in facilitating transactions for digital assets and the challenges it faces in becoming a widely accepted payment asset.

Now, why did it catch me off guard? Primarily, it feels like a reiteration of the ongoing discourse in the crypto community. They haven't ventured beyond the surface, merely echoing what has been resonating in the crypto space for a while now.

Moreover, I found a glaring omission in their analysis regarding Bitcoin's long-term viability. The community has been buzzing about the potential sustainability issues Bitcoin might face due to its rigid 21 million cap.

The transaction fees alone might not suffice to keep the miners motivated in the long run.

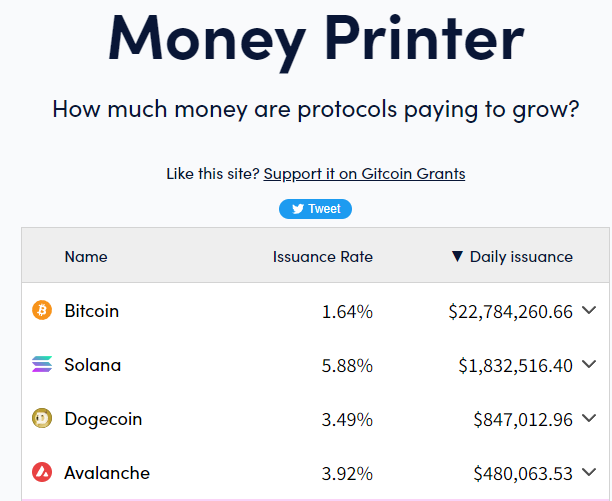

It's startling to note that Bitcoin generates fewer fees than Aave, yet mints a whopping 22.7M daily. What’s it called when you print 22.7M and receive 500K a day? Hm, ponzinomics?

At this juncture, Bitcoin seems to be riding primarily on its monetary premium.

This is a great discussion in case you want to dig deeper. Justin Bons is the pro-Ethereum and Eric Wall is the pro-Bitcoin. Needless to say, I respect the shit out of Eric, even though I side with Justin.

Let’s continue:

Fidelity posits: "ether shares many properties of money with bitcoin and other currencies; however, it diverges significantly in terms of scarcity and historical trajectory."

While Ethereum embraces frequent upgrades, a strategy grounded in foresight, Bitcoin might eventually find itself at a crossroads, possibly compromising its famed scarcity and track record.

Nevertheless, Fidelity’s thesis does hit the mark in certain aspects, acknowledging Ethereum's distinctive edge in facilitating complex transactions, thereby carving out a unique, money-esque utility that warrants consideration.

They also rightly pointed out the current dynamics of the stock-to-flow ratio, where Ether has surpassed Bitcoin as of July 2023.

So, while the thesis aligns with some prevalent narratives, it perhaps missed an opportunity to delve deeper and present a more nuanced analysis.

Personal note: I’m still trying to find the perfect niche for my newsletter. What are you most interested in? What do you think is missing in the space? Reach out! Put a comment here or send me a DM on X (Twitter).